Renewable Energy Sector in India keep Growing Despite Challenges Posed by COVID-19 Pandemic

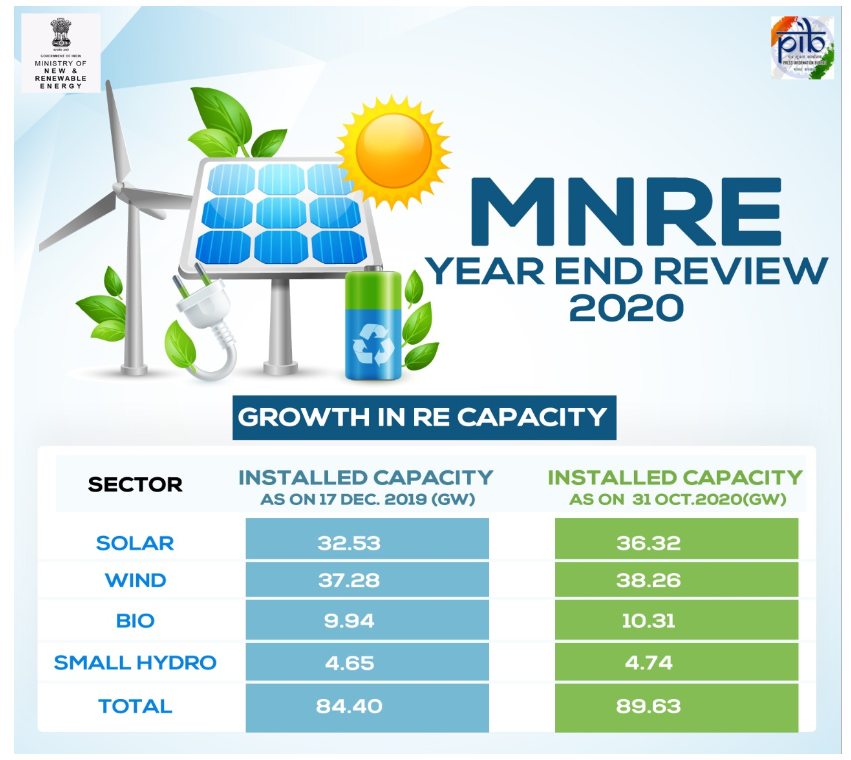

Installed RECapacity reaches over 89.63 GW in October, 2020

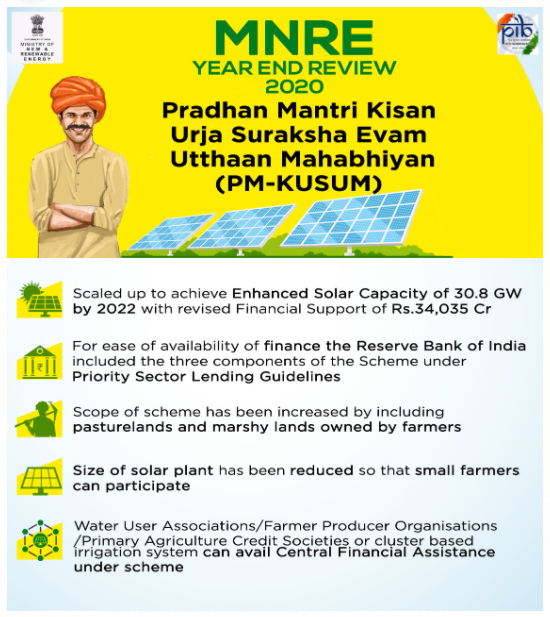

PM-KUSUM Scaled up to achieve Enhanced Solar Capacity of 30.8 GW by 2022 with revised Financial Support of Rs.34,035 Cr

PLI Scheme for Manufacturing of High Efficiency Modules Approved by Cabinet to promote Domestic Manufacturing in RE Sector

1.0 Introduction

Government of India has been driving a vibrant renewable energy programme aimed at achieving energy security, energy access and reducing the carbon footprints of the national economy. This is in line with India’s commitments under the 2015 Paris Agreement to reduce greenhouse gas emissions intensity by 33 to 35 percent below 2005 levels, and to achieve 40 percent of installed electric power capacity from non-fossil sources by 2030. With progressively declining costs, improved efficiency and reliability renewable energy is now an attractive option for meeting the energy needs across different sectors of the economy. However, renewable energy technologies are still evolving in terms of technological maturity and cost competitiveness, and face numerous market related, economic and social barriers.

Keeping in view the above and our commitment for a healthy planet with less carbon intensive economy, we decided in 2015 that 175 GW of renewable energy capacity will be installed by the year 2022. This includes 100 GW from solar, 60 GW from wind, 10 GW from biomass and 5 GW from small hydro power.With the accomplishment of these ambitious targets, India will become one of the largest Green Energy producers in the world, surpassing several developed countries.

2.0 Achievements

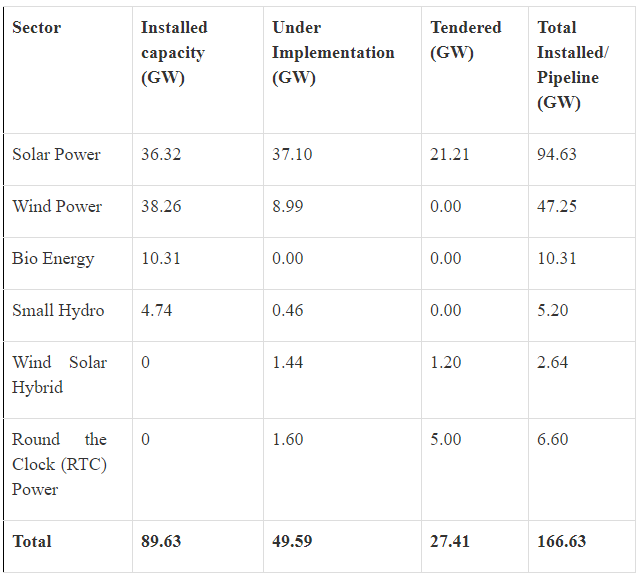

As on 31st October 2020, India’s total renewable energy installed capacity (excluding hydro power above 25 MW) had reached over 89.63 GW. During the last 6 years, India has witnessed the fastest rate of growth in renewable energy capacity addition among all large economies, with renewable energy capacity growing by 2.5 times and solar energy expanding by over 13 times.Renewable energy now constitutes over 24 per cent of the country’s installed power capacity and around 11.62 per cent of the electrical energy generation. If large hydro is included, the share of renewable energy in electric installed capacity would be over 36 percent and over 26 per cent of the electric energy generation. Around 49.59 GW renewable energy capacity is under installation, and an additional 27.41 GW capacity has been tendered. This makes the total capacity that is already commissioned and in the pipe line about 166.63 GW. Further, large hydro power, which has also been declared as renewable energy has about 45 GW hydro installed capacity and 13 GW capacity under installation. This brings our total renewable energy portfolio of installed and in pipeline projects to 221 GW. Sector wise details of Installed Capacity from renewables excluding large hydro above 25 MW is as follows:

4.0 Policies/Major initiative/Schemes/Programmes for accelerated uptake of Renewables

4.1 Major Programmes and Schemes:

4.1.1 National Solar Mission (NSM)

Harnessing solar energy is one the major component of India’s renewable energy strategy. Most parts of India receive abundant solar radiation and the country has an estimated solar energy potential of about 750 GW solar power. In January 2010, the NSM was launched with the objective of establishing India as a global leader in solar energy, by creating the policy conditions for solar technology diffusion across the country as quickly as possible.

The initial target of NSM was to install 20 GW solar power by 2022. This was upscaled to 100 GW in early 2015. Numerous facilitative programmes and schemes under the Mission have driven the grid connected solar power installed capacity from 25 MW in the year 2010-11 to about 36.32 GW as on 31st October 2020. An additional 58.31 GW solar power capacity is currently under installation/ tendering process.

-

Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM):

PM-KUSUM Scheme is an ambitious scheme consisting of three components for providing water and energy security to farmers and enhancing their income by making Annadata also aUrjadata. During the budget for 2020-21 expansion of scheme was announced to increase quantity of standalone solar pumps covered under the scheme from 17.5 lakh to 20 lakh pumps and quantity of solarisation of grid connected pumps from 10 lakh to 15 lakh. With expansion the target solar capacity under the Scheme has increased to 30.8 GW from earlier 25.8 GW. Due to COVID-19 the implementation was slow during first half of the year, however, progress picked-up from August 2020 onwards. Based on the learning during first year, provisions for feeder level solarisation are being included in the scheme. Convergence of Scheme with PM-KSY and Agriculture Infrastructure Fund has also been provided for. For ease of availability of finance the Reserve Bank of India included the three components of the Scheme under Priority Sector Lending Guidelines. Cumulatively 5000 MW small solar power plants, 7 lakh standalone solar pumps and solarisation of 4 lakh grid connected pumps are targeted for sanction during 2020-21.

In November, 2020, MNRE amended/clarified implementation Guidelines of Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyaan (PM-KUSUM) Scheme based on the learnings from the implementation of the Scheme during the first year. Scope of scheme has been increased by including pasturelands and marshy lands owned farmers. Size of solar plant has been reduced so that small farmers can participate and completion period increased from nine to twelve months. Further, penalty for shortfall in generation removed for ease of implementation by farmers.As per the same MNRE order, Central Financial Allowance (CFA) willbe allowed for solar pumps to be set up and used by Water User Associations (WUAs)/Farmer Producer Organisations (FPOs)/Primary Agriculture Credit Societies (PACSs) or for cluster based irrigationsystem along with individual farmers.

II. Off-Grid Solar PV Applications Programme Phase III: Implementation of Phase-3 of the Off-Grid Solar PV Applications Programme for Solar Street Lights, Solar Study Lamps and Solar Power Packs was extended for North-Eastern States during the year. Sanction under the Scheme stands at 1.74 lakh solar street lights, 13.5 lakh solar study lamps and 4 MW capacity solar power packs, which in under different stages of implementation by state nodal agencies. Till October 2020 around 30000 solar street lights installed, 2.13 lakh solar study lamps distributed and 1.5 MW solar power packs have been set-up as reported by SNAs.

III. Atal Jyoti Yojana (AJAY) Phase-II: The AJAY Ph-II Scheme for installation of solar street lights with 25% fund contribution from MPLAD Funds was discontinued from 1 April 2020 as the Government decided to suspend the MPLAD Funds for next two years i.e. 2020-21 and 2021-22. However, installation of 1.5 lakh solar street lights sanctioned under the scheme till March 2020 was under progress and till October 2020 around 0.84 lakh solar street lights reported installed and balance are targeted to be completed by March 2021.

-

Roof Top Solar programme Phase-II: Roof Top Solar programme Phase-II for accelerated deployment of solar roof top systems with a target of 40 GW installed capacity by the year 2021-22, is also under implementation. The scheme provides for financial incentive for 4 GW of solar roof top capacity to residential sector and there is a provision to incentivise the distribution companies for incremental achievement over the previous year. For residential sector use of domestically manufactured solar cells and modules have been mandated. This scheme is expected to act as catalyst for adding solar cell and module manufacturing capacity in India. So far, a cumulative 4.4 GW solar roof top projects have been set up in the country.

V. Solar Parks Scheme: To facilitate large scale grid connected solar power projects, a scheme for “Development of Solar Parks and Ultra Mega Solar Power Projects” is under implementation with a target capacity of 40 GW capacity by March 2022. Solar parks provide solar power developers with a plug and play model, by facilitating necessary infrastructure like land, power evacuation facilities, road connectivity, water facility etc. along with all statuary clearances. So far, 40 solar parks have been sanctioned with a cumulative capacity of 26.3 GW in 15 states. Solar power projects of an aggregate capacity of around 8 GW have already been commissioned in these parks.

VI. Public Sector Undertaking (CPSU) Scheme: A scheme for setting up 12 GW Grid- Connected Solar PV Power Projects by Public Sector Undertakings with domestic cells and modules is under implementation. Viability Gap Funding support is provided under this scheme. Apart from adding solar capacity, the scheme will also create demand for domestically manufactured solar cells/modules, and thus help domestic manufacturing.

4.1.2 Wind Power

India’s wind power potential at hub height of 120 meters is 695 GW. The wind power installed capacity has grown by 1.8 times during past 6.5 years to about 38.26 GW (as on 31st October 2020) and India now has the 4th largest wind power capacity in the world. The wind energy sector is led by the indigenous wind power industry with a strong project ecosystem, operation capabilities and a manufacturing base of about 10 GW per annum. Ministry is developing strategy and roadmap to harness the potential of offshore wind energy along India’s coastline.

-

Scheme for procurement of blended wind power from 2500 MW ISTS connected projects

The objective of the Scheme is to provide a framework for procurement of electricity from 2500 MW ISTS Grid Connected Wind Power Projects with up to 20% blending with Solar PV Power through a transparent process of bidding. Solar Energy Corporation of India Ltd. (SECI) is the nodal agency for implementation of the Scheme. It has provisions for payment security mechanism, commission schedule, power offtake constraints, power purchase agreement, etc. SECI has awarded 970 MW of projects under this scheme at discovered tariff of Rs. 2.99-3.00 per unit.

-

Guidelines for Tariff Based Competitive Bidding Process for procurement of power from Grid Connected Wind Solar Hybrid Projects

The objective is to provide a framework for procurement of electricity from ISTS Grid Connected Wind-Solar Hybrid Power Projects through a transparent process of bidding. Individual minimum size of project allowed is 50 MW at one site and a single bidder cannot bid for less than 50 MW. The rated power capacity of one resource (wind or solar) shall be at least 33% of the total contracted capacity. It has provisions for payment security mechanism, commission schedule, power offtake constraints, power purchase agreement, etc. SECI is the nodal agency for implementation of the Scheme.

4.1.3 Other renewables for power generation

The Ministry is implementing a scheme to support biomass-based co-generation in sugar mills and other industries. Energy generation from urban, industrial, and agricultural waste/residues is an area of focus. Waste to Energy projects, besides generating useful energy, also help combat pollution. As on 31stOctober 2020, installed capacity of grid connected biomass power projects stood at about 10.15 GW, waste to energy projects capacity was 168.64 MW (grid connected) and 204.73 MWeq (off grid), and about 4.74 GW small hydro power capacity from 1133 small hydro power projects was operational.

4.1.4 Green Energy Corridor

In order to facilitate renewable power evacuation and reshaping the grid for future requirements, the Green Energy Corridor (GEC) projects have been initiated. The first component of the scheme, Inter-state GEC with target capacity of 3200 circuit kilometer (ckm) transmission lines and 17,000 MVA capacity sub-stations, was completed in March 2020. The second component – Intra-state GEC with a target capacity of 9700 ckm transmission lines and 22,600 MVA capacity sub-stations is expected to be completed by May 2021. The present efforts are focused on strengthening institutions, resources and protocols, and investing judiciously in grid infrastructure. A total of 7175 ckm of transmission lines have been constructed and substations of aggregated capacity of 7825 MVA have been charged.

4.2 Policies and Initiatives:

India has worked systemically for putting in place facilitative policies and programmes for achieving the goal. The success is mainly attributed to several diverse policy instruments, as under:-

-

To create a pan-India renewable energy market and encourage setting up of the renewable energy projects in high renewable resource potential areas, in September 2016, waiver of Inter State Transmission System charges and losses for sale of power from solar and wind power projects was notified. This waiver has been extended to projects to be commissioned up to 30 June 2023.

-

Keeping in view India’s long-term goals of decarbonising the electricity systems, and achieving energy security, and in keeping with our international commitments, in July 2016, long term Renewable Purchase Obligation growth trajectory, uniformly applicable to all States/UTs, was notified.

-

Competitive Bidding guidelines for procurement of solar and wind power have been notified under section 63 of Electricity Act, 2003. These Guidelines provide for standardization and uniformity of the procurement process and a risk-sharing framework between various stakeholders, thereby encouraging investments, enhancing bankability of projects and improving profitability. The Guidelines also facilitate transparency and fairness in the procurement processes which have resulted in the drastic fall in solar and wind power prices over the past few years

-

Solar rooftop systems have been promoted in commercial /industrial/Govt. sector /residential sector through policy and regulatory interventions e.g. mandatory solar provision in the Model Building bye-laws of MoHUA and concessional financing arrangement through Banks/FIs in addition to central financial assistance for residential sector and achievement based incentives to DISCOMs. In addition few States has also made provision of mandatory solar installation for buildings above certain plot area/connected load.

-

Foreign investors can enter into joint venture with an Indian partner for financial and/or technical collaboration and for setting up of renewable energy-based power generation projects. Upto 100 per cent foreign investment as equity qualifies for automatic approval.

-

To build investor trust by ensuring payment security and tackle the risks related to delays in payments to independent power producers, DISCOMs have been mandated to issue and maintain letter of credit (LCs);

-

For quality assurance, standards for deployment of solar photovoltaic systems/devices have been notified.

-

Renewable energy projects have been given priority sector lending status for loans up to a limit of Rs 30 crore.

-

Off-grid applications are promoted through provision of subsidies from the central government.

-

Efforts have been undertaken to strengthen and expand the domestic manufacturing eco-system. Schemes namely PM-KUSUM, Solar Rooftop and CPSU have a precondition of Domestic Content Requirement, directly creating a domestic demand of more than 36 GW solar PV (cells & modules). In order to curb proliferation of imported solar PV cells and modules, a Safeguard Duty was imposed w.e.f. 30 July 2018 for two years. It has been extended for one more year at the rates of 14.90 per cent for imports during 30 July, 2020 to 29 January, 2021; and 14.50 percent for imports during 30th January, 2021 to 29th July, 2021. Imposition of an enhanced Basic Customs Duty and financial incentives for domestic solar PV manufacturing have also been envisaged

5.0 Issues/Challenges ahead

India is confronted with major challenges in moving towards higher deployment levels for renewables. Some of these are listed below-

5.1 Mobilization of the necessary finance and investment on competitive terms: Gearing up the banking sector for arranging finances for larger deployment goals, exploring low-interest rate, long-term international funding, and developing a suitable mechanism for risk mitigation or sharing by addressing both technical and financial bottlenecks are major challenges. The ongoing efforts for mitigating investment risks, and easing approval processes would also need to be strengthened.

5.2 Land acquisition: Land acquisition is one of the major challenges in renewable power development. Identification of land with RE potential, its conversion (if needed), clearance from land ceiling act, decision on land lease rent, clearance from revenue department, and other such clearances take time. State governments have to play a major role in acquisition of land for RE projects.

5.3 Creating an innovation and manufacturing eco-system in the country;

5.4 Economically integrating larger share of renewables with the grid;

5.5 Enabling supply of firm and dispatchable power from renewables;

5.6 Enabling penetration of renewables in the so called hard to decarbonize sectors.

6.0 Impact of Covid-19

6.1 The COVID-19 pandemic has thrown up tough challenges. The pace of renewable energy projects development and commissioning has been impacted. However, the Ministry was quick to respond to the situation. The operation of renewable energy generation plants was declared as an essential service, and a policy for granting extension of time for various renewable energy projects treating the lockdown as force majeure has been put in place. The bidding for new projects has also continued unimpeded, despite the pandemic and lockdown.

6.2 The following major steps/ measures were taken during COVID to facilitate ease of doing business:-

6.2.1 Instructions were issued for granting time extension to renewable energy projects and release of performance bank guarantees proportionate to work completion, to mitigate the impact of COVID-19;

6.2.2 States have been advised to maintain sanctity of contracts and ensure certainty in supporting policies for renewables;

6.2.3 It has been clarified to the States that ‘must run ‘status of renewable energy remains unchanged during the lockdown period, and that curtailment, except for grid safety reasons, would amount to deemed generation;

6.2.4 Suitable relief/extension was granted in all time-bound activities which were affected by the pandemic.

7.0 Steps to promote domestic manufacturing in Renewable Energy sector(Aatmanirbhar Bharat Policy)

-

Domestic Content Requirement (DCR):

CPSU Scheme Phase-II (12 GW), PM- KUSUM (20.8 GW) and Grid-connected Rooftop Solar Program Phase-II (4 GW) – In 36.8 GW of projects, use of domestically manufactured Solar Cells & Modules is mandatory.

-

‘Preference to Make in India Order’

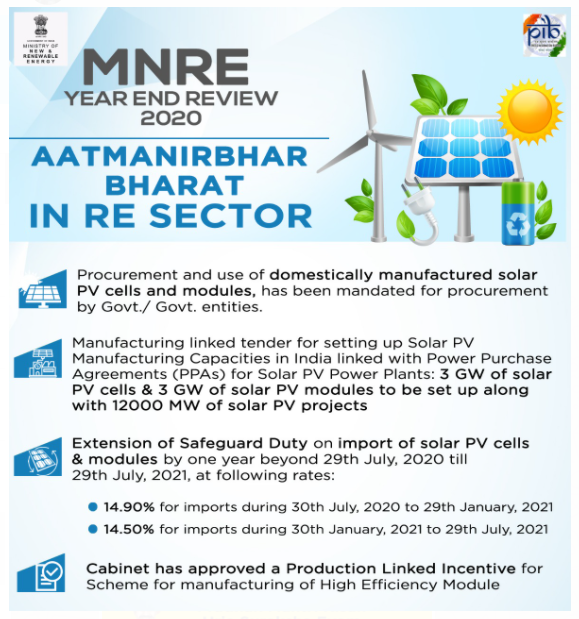

Procurement and use of domestically manufactured solar PV cells and modules, has been mandated for procurement by Govt./ Govt. entities.

-

Manufacturing linked tender for setting up Solar PV Manufacturing Capacities in India linked with Power Purchase Agreements (PPAs) for Solar PV Power Plants: 3 GW of solar PV cells & 3 GW of solar PV modules to be set up along with 12000 MW of solar PV projects. LoA issued. Manufacturing plants will be set up in the next 2 years

7.4 Extension of Safeguard Duty on import of solar PV cells & modules by one year beyond 29th July, 2020 till 29th July, 2021, at following rates:

-

14.90% for imports during 30th July, 2020 to 29th January, 2021;

-

14.50% for imports during 30th January, 2021 to 29th July, 2021;

-

Imposition of Basic Customs Duty (BCD) on import of solar PV cells, solar PV modules and solar inverters:

MNRE, has sent a proposal to Ministry of Finance for phased imposition of Basic Customs Duty (BCD) on import of solar PV cells, solar PV modules and solar inverters.- under consideration

7.6 New Manufacturing PLI Scheme:

The Cabinet has approved a Production Linked Incentive for Scheme for manufacturing of High Efficiency Module. The EFC note is under finalisation.

-

Country is truly Atmanirbhar in wind power sector: Around 70-80% indigenization has been achieved with strong domestic manufacturing in the wind sector. All the major global players in this field have their presence and over 40 different models of wind turbines are being manufactured by 17 different companies, through (i) joint ventures under licensed production (ii) subsidiaries of foreign companies, and (iii) Indian companies with their own technology. The unit size of machines has gone up to 3.00 MW. The current annual production capacity of wind turbines in the country is about 8000 MW to 10000 MW.

-

Manufacturing Zone for Power and RE equipment: MNRE & MoP are working on a scheme for setting up manufacturing Zones in different regions. States will be selected on the basis of their offer. The manufacturers will get hassle free land and best prices for land, power and water charges, state incentives etc.

-

The Ministry is also finalising a list of Capital Machineries so that they get Exemption of duty on imports required for setting up a manufacturing plant.

-

Project Development Cell (PDC) has been established to handhold and facilitates domestic and foreign investors. PDC is reaching out to potential investors who are willing to set up manufacturing capacities in India;

7.11 Foreign Direct Investment (FDI) cell has been created in the Ministry in line with DPIIT recommendations for curbing opportunistic takeovers/acquisitions of Indian companies due to current COVID-19 pandemic.

*********